Forget Nuclear

By Amory B. Lovins, Imran Sheikh, and Alex Markevich

Rocky Mountain Institute

April 28, 2008

Correction Appended

Nuclear power, we’re told, is a vibrant industry that’s dramatically

reviving because it’s proven, necessary, competitive, reliable, safe,

secure, widely used, increasingly popular, and carbon-free—a perfect

replacement for carbon-spewing coal power. New nuclear plants thus

sound vital for climate protection, energy security, and powering a

growing economy.

There’s a catch, though: the private capitalmarket isn’t investing

in new nuclear plants, and without financing, capitalist utilities

aren’t buying. The few purchases, nearly all in Asia, are all made by

central planners with a draw on the public purse. In the United States,

even government subsidies approaching or exceeding new nuclear power’s

total cost have failed to entice Wall Street.

This non-technical summary article compares the cost, climate

protection potential, reliability, financial risk, market success,

deployment speed, and energy contribution of new nuclear power with

those of its low- or no-carbon competitors. It explains why soaring

taxpayer subsidies aren’t attracting investors. Capitalists instead

favor climate-protecting competitors with less cost, construction time,

and financial risk. The nuclear industry claims it has no serious

rivals, let alone those competitors—which, however, already outproduce

nuclear power worldwide and are growing enormously faster.

Most remarkably, comparing all options’ ability to protect the

earth’s climate and enhance energy security reveals why nuclear power

could never deliver these promised benefits even if it could find

free-market buyers—while its carbon-free rivals, which won $71 billion

of private investment in 2007 alone, do offer highly effective climate

and security solutions, sooner, with greater confidence.

Uncompetitive Costs

The Economist

observed in 2001 that “Nuclear power, once claimed to be too cheap to

meter, is now too costly to matter”—cheap to run but very expensive to

build. Since then, it’s become several-fold costlier to build, and in a

few years, as old fuel contracts expire, it is expected to become

several-fold costlier to run. Its total cost now markedly exceeds that

of other common power plants (coal, gas, big wind farms), let alone the

even cheaper competitors described below.

Construction costs worldwide have risen far faster for nuclear than

non-nuclear plants, due not just to sharply higher steel, copper,

nickel, and cement prices but also to an atrophied global

infrastructure for making, building, managing, and operating reactors.

The industry’s flagship Finnish project, led by France’s top builder,

after 28 months’ construction had gone at least 24 months behind

schedule and $2 billion over budget.

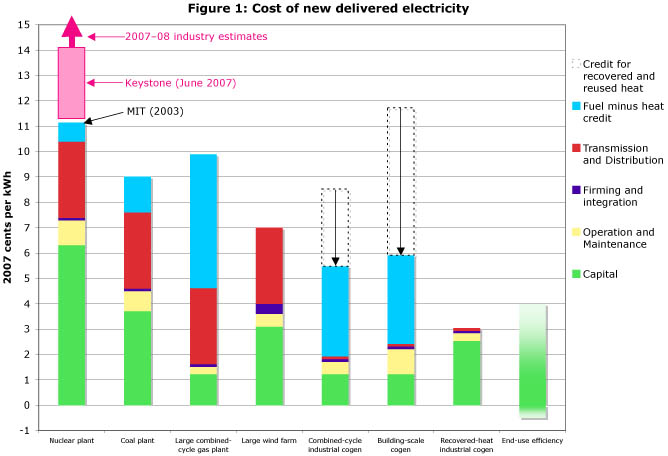

By 2007, as Figure 1 shows, nuclear was the costliest option among

all main competitors, whether using MIT’s authoritative but now low

2003 cost assessment1, the Keystone Center’s mid-2007 update

(see Figure 1, pink bar), or later and even higher industry estimates

(see Figure 1, pink arrow)2.

Cogeneration and efficiency are “distributed resources,” located

near where energy is used. Therefore, they don’t incur the capital

costs and energy losses of the electric grid, which links large power

plants and remote wind farms to customers3. Wind farms, like solar cells4,

also require “firming” to steady their variable output, and all types

of generators require some backup for when they inevitably break. The

graph reflects these costs.

Making electricity from fuel creates large amounts of byproduct

heat that’s normally wasted. Combined-cycle industrial cogeneration and

buildingscale cogeneration recover most of that heat and use it to

displace the need for separate boilers to heat the industrial process

or the building, thus creating the economic “credit” shown in Figure 1.

Cogenerating electricity and some useful heat from currently discarded

industrial heat is even cheaper because no additional fuel is needed5.

End-use efficiency lets customers wring more service from each

kilowatthour by using smarter technologies. As RMI’s work with many

leading firms has demonstrated, efficiency provides the same or better

services with less carbon, less operating cost, and often less up-front

investment. The investment required to save a kilowatt-hour averages

about two cents nationwide, but has been less than one cent in hundreds

of utility programs (mainly for businesses), and can even be less than

zero in new buildings and factories—and in some retrofits that are

coordinated with routine renovations.

Wind, cogeneration, and end-use efficiency already provide

electrical services more cheaply than central thermal power plants,

whether nuclear- or fossil-fuelled. This cost gap will only widen,

since central thermal power plants are largely mature while their

competitors continue to improve rapidly. The high costs of conventional

fossil-fuelled plants would go even higher if their large carbon

emissions had to be captured.

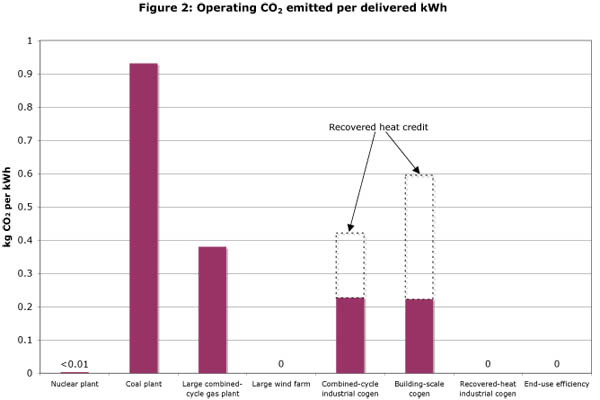

Uncompetitive CO2 Displacement

Nuclear plant operations emit almost no carbon—just a little to produce the fuel under current conditions6.

Nuclear power is therefore touted as the key replacement for coal-fired

power plants. But this seemingly straightforward substitution could

instead be done using non-nuclear technologies that are cheaper and

faster, so they yield more climate solution per dollar and per year. As

Figure 2 shows, various options emit widely differing quantities of CO2

per delivered kilowatt-hour.

Coal is by far the most carbonintensive source of electricity, so

displacing it is the yardstick of carbon displacement’s effectiveness.

A kilowatthour of nuclear power does displace nearly all the 0.9-plus

kilograms of CO2 emitted by producing a kilowatt-hour from coal. But so

does a kilowatthour from wind, a kilowatt-hour from recovered-heat

industrial cogeneration, or a kilowatt-hour saved by end-use

efficiency. And all of these three carbonfree resources cost at least

one-third less than nuclear power per kilowatt-hour, so they save more

carbon per dollar.

Combined-cycle industrial cogeneration and building-scale

cogeneration typically burn natural gas, which does emit carbon (though

half as much as coal), so they displace somewhat less net carbon than

nuclear power could: around 0.7 kilograms of CO2 per kilowatt-hour7.

Even though cogeneration displaces less carbon than nuclear does per

kilowatt-hour, it displaces more carbon than nuclear does per dollar

spent on delivered electricity, because it costs far less. With a net

delivered cost per kilowatthour approximately half of nuclear’s,

cogeneration delivers twice as many kilowatt-hours per dollar, and

therefore displaces around 1.4 kilograms of CO2 for the same cost as

displacing 0.9 kilograms of CO2 with nuclear power.

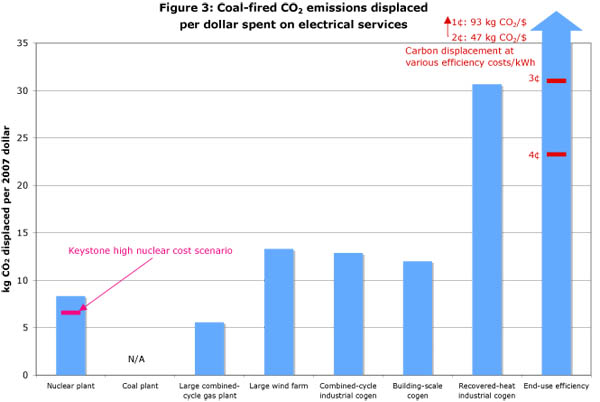

Figure 3 compares different electricity options’ cost-effectiveness

in reducing CO2 emissions. It counts both their cost-effectiveness, in

delivering kilowatthours per dollar, and their carbon emissions, if any.

Nuclear power, being the costliest option, delivers less electrical

service per dollar than its rivals, so, not surprisingly, it’s also a

climate protection loser, surpassing in carbon emissions displaced per

dollar only centralized, non-cogenerating combined-cycle power plants

burning natural gas8. Firmed windpower and cogeneration are

1.5 times more costeffective than nuclear at displacing CO2. So is

efficiency at even an almost unheard-of seven cents per kilowatthour.

Efficiency at normally observed costs beats nuclear by a wide margin—

for example, by about ten-fold for efficiency costing one cent per

kilowatthour.

New nuclear power is so costly that shifting a dollar of spending

from nuclear to efficiency protects the climate several-fold more than

shifting a dollar of spending from coal to nuclear. Indeed, under

plausible assumptions, spending a dollar on new nuclear power instead

of on efficient use of electricity has a worse climate effect than

spending that dollar on new coal power!

If we’re serious about addressing climate change, we must invest

resources wisely to expand and accelerate climate protection. Because

nuclear power is costly and slow to build, buying more of it rather

than of its cheaper, swifter rivals will instead reduce and retard

climate protection.

Questionable Reliability

All sources of

electricity sometimes fail, differing only in why, how often, how much,

for how long, and how predictably. Even the most reliable giant power

plants are intermittent: they fail unexpectedly in billion-watt chunks,

often for long periods. Of all 132 U.S. nuclear plants built (52

percent of the 253 originally ordered), 21 percent were permanently and

prematurely closed due to reliability or cost problems, while another

27 percent have completely failed for a year or more at least once.

Even reliably operating nuclear plants must shut down, on average, for

39 days every 17 months for refueling and maintenance. To cope with

such intermittence in the operation of both nuclear and centralized

fossil-fuelled power plants, which typically fail about 8 percent of

the time, utilities must install a roughly 15 percent “reserve margin”

of extra capacity, some of which must be continuously fuelled, spinning

ready for instant use. Heavily nuclear-dependent regions are

particularly at risk because drought, a serious safety problem, or a

terrorist incident could close many plants simultaneously.

Nuclear plants have an additional disadvantage: for safety, they

must instantly shut down in a power failure, but for nuclear-physics

reasons, they can’t then be quickly restarted. During the August 2003

Northeast blackout, nine perfectly operating U.S. nuclear units had to

shut down. Twelve days of painfully slow restart later, their average

capacity loss had exceeded 50 percent. For the first three days, just

when they were most needed, their output was below 3 percent of normal.

The big transmission lines that highly concentrated nuclear plants

require are also vulnerable to lightning, ice storms, rifle bullets,

and other interruptions. The bigger our power plants and power lines

get, the more frequent and widespread regional blackouts will become.

Because 98–99 percent of power failures start in the grid, it’s more

reliable to bypass the grid by shifting to efficiently used, diverse,

dispersed resources sited at or near the customer. Also, a portfolio of

many smaller units is unlikely to fail all at once: its diversity makes

it especially reliable even if its individual units are not.

The sun doesn’t always shine on a given solar panel, nor does the

wind always spin a given turbine. Yet if properly firmed, both

windpower, whose global potential is 35 times world electricity use,

and solar energy, as much of which falls on the earth’s surface every

~70 minutes as humankind uses each year, can deliver reliable power

without significant cost for backup or storage. These variable

renewable resources become collectively reliable when diversified in

type and location and when integrated with three types of resources:

steady renewables (geothermal, small hydro, biomass, etc.), existing

fuelled plants, and customer demand response. Such integration uses

weather forecasting to predict the output of variable renewable

resources, just as utilities now forecast demand patterns and

hydropower output. In general, keeping power supplies reliable despite

large wind and solar fractions will require less backup or storage

capacity than utilities have already bought to manage big thermal

stations’ intermittence. The myth of renewable energy’s unreliability

has been debunked both by theory and by practical experience. For

example, three north German states in 2007 got upwards of 30% of their

electricity from windpower-39% in Schleswig-Holstein, whose goal is

100% by 2020.

Large Subsidies to Off set High Financial Risk

The latest U.S. nuclear plant proposed is estimated to cost $12–24

billion (for 2.2–3.0 billion watts), many times industry’s claims, and

off the chart in Figure 1 above. The utility’s owner, a large holding

company active in 27 states, has annual revenues of only $15 billion.

Such high, and highly uncertain, costs now make financing prohibitively

expensive for free-market nuclear plants in the half of the U.S. that

has restructured its electricity system, and prone to politically

challenging rate shock in the rest: a new nuclear kilowatt-hour

costing, say, 16 cents “levelized” over decades implies that the

utility must collect ~27 cents to fund its first year of operation.

Lacking investors, nuclear promoters have turned back to taxpayers,

who already bear most nuclear accident risks and have no meaningful say

in licensing. In the United States, taxpayers also insure operators

against legal or regulatory delays and have long subsidized existing

nuclear plants by ~1–5¢ per kilowatt-hour. In 2005, desperate for

orders, the politically potent nuclear industry got those subsidies

raised to ~5–9¢ per kilowatthour for new plants, or ~60–90 percent of

their entire projected power cost. Wall Street still demurred. In 2007,

the industry won relaxed government rules that made its 100 percent

loan guarantees (for 80 percent-debt financing) even more

valuable—worth, one utility’s data revealed, about $13 billion for a

single new plant. But rising costs had meanwhile made the $4 billion of

new 2005 loan guarantees scarcely sufficient for a single reactor, so

Congress raised taxpayers’ guarantees to $18.5 billion. Congress will

be asked for another $30+ billion in loan guarantees in 2008.

Meanwhile, the nonpartisan Congressional Budget Office has concluded

that defaults are likely.

Wall Street is ever more skeptical that nuclear power is as

robustly competitive as claimed. Starting with Warren Buffet, who just

abandoned a nuclear project because “it does not make economic sense,”

the smart money is heading for the exits. The Nuclear Energy Institute

is therefore trying to damp down the rosy expectations it created. It

now says U.S. nuclear orders will come not in a tidal wave but in two

little ripples—a mere 5–8 units coming online in 2015–16, then more if

those are on time and within budget. Even that sounds dubious, as many

senior energyindustry figures privately agree. In today’s capital

market, governments can have only about as many nuclear plants as they

can force taxpayers to buy.

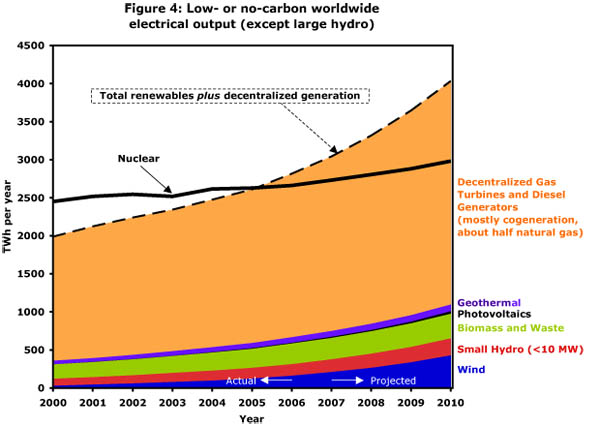

The Micropower Revolution

While nuclear power

struggles in vain to attract private capital, investors have switched

to cheaper, faster, less risky alternatives that The Economist

calls “micropower”—distributed turbines and generators in factories or

buildings (usually cogenerating useful heat), and all renewable sources

of electricity except big hydro dams (those over ten megawatts). These

alternatives surpassed nuclear’s global capacity in 2002 and its

electric output in 2006. Nuclear power now accounts for about 2 percent

of worldwide electric capacity additions, vs. 28 percent for micropower

(2004– 07 average) and probably more in 2007–08.

An even cheaper competitor is enduse efficiency

(“negawatts”)—saving electricity by using it more effi ciently or at

smarter times. Despite subsidies generally smaller than nuclear’s, and

many barriers to fair market entry and competition, negawatts and

micropower have lately turned in a stunning global market performance.

Micropower’s actual and industry-projected electricity production is

running away from nuclear’s, not even counting the roughly comparable

additional growth in negawatts, nor any fossil-fuelled generators under

a megawatt (see Figure 4)9.

The nuclear industry nonetheless claims its only serious

competitors are big coal and gas plants. But the marketplace has

already abandoned that outmoded battleground for two others: central

thermal plants vs. micropower, and megawatts vs. negawatts. For

example, the U.S. added more windpower capacity in 2007 than it added

coal-fired capacity in the past five years combined. By beating all

central thermal plants, micropower and negawatts together provide about

half the world’s new electrical services. Micropower alone now provides

a sixth of the world’s electricity, and from a sixth to more than half

of all electricity in twelve industrial countries (the U.S. lags with 6

percent).

In this broader competitive landscape, high carbon prices or taxes

can’t save nuclear power from its fate. If nuclear did compete only

with coal, then far above- market carbon prices might save it; but coal

isn’t the competitor to beat. Higher carbon prices will advantage all

other zero-carbon resources—renewables, recoveredheat cogeneration, and

negawatts—as much as nuclear, and will partly advantage fossil-fueled

but low-carbon cogeneration as well.

Small Is Fast, Low-Risk, and High in Total Potential

Small, quickly built units are faster to deploy for a given total

effect than a few big, slowly built units. Widely accessible choices

that sell like cellphones and PCs can add up to more, sooner, than

ponderous plants that get built like cathedrals. And small units are

much easier to match to the many small pieces of electrical demand.

Even a multimegawatt wind turbine can be built so quickly that the U.S.

will probably have a hundred billion watts of them installed before it

gets its fi rst one billion watts of new nuclear capacity, if any.

Small, quickly built units also have far lower financial risks than

big, slow ones. This gain in financial economics is the tip of a very

large iceberg: micropower’s more than 200 different kinds of hidden fi

nancial and technical benefits can make it about ten times more

valuable (www.smallisprofitable.org) than implied by current prices or by the cost comparisons above. Most of the same benefits apply to negawatts as well.

Despite their small individual size, micropower generators and

electrical savings are already adding up to huge totals. Indeed, over

decades, negawatts and micropower can shoulder the entire burden of

powering the economy.

The Electric Power Research Institute (EPRI), the utilities’

think-tank, has calculated the U.S. negawatt potential (cheaper than

just running an existing nuclear plant and delivering its output) to be

two to three times nuclear power’s 19 percent share of the U.S.

electricity market; RMI’s more detailed analysis found even more.

Cogeneration in factories can make as much U.S. electricity as nuclear

does, plus more in buildings, which use 69 percent of U.S. electricity.

Windpower at acceptable U.S. sites can cost-effectively produce at

least twice the nation’s total electricity use, and other renewables

can make even more without significant land-use, variability, or other

constraints. Thus just cogeneration, windpower, and efficient use—all

profitable—can displace nuclear’s current U.S. output roughly 14 times

over.

Nuclear power, with its decade-long project cycles, difficult

siting, and (above all) unattractiveness to private capital, simply

cannot compete. In 2006, for example, it added less global capacity

than photovoltaics did, or a tenth as much as windpower added, or 30–41

times less than micropower added. Renewables other than big hydro dams

won $56 billion of private risk capital; nuclear, as usual, got zero.

China’s distributed renewable capacity reached seven times its nuclear

capacity and grew seven times faster. And in 2007, China, Spain, and

the U.S. each added more windpower capacity than the world added

nuclear capacity. The nuclear industry does trumpet its growth, yet

micropower is bigger and growing 18 times faster.

Security Risks

President Bush rightly

identifies the spread of nuclear weapons as the gravest threat to

America. Yet that proliferation is largely driven and greatly

facilitated by nuclear power‘s flow of materials, equipment, skills,

and knowledge, all hidden behind its innocent-looking civilian

disguise. (Reprocessing nuclear fuel, which the President hopes to

revive, greatly complicates waste management, increases cost, and

boosts proliferation.) Yet acknowledging nuclear power’s market failure

and moving on to secure, least-cost energy options for global

development would unmask and penalize proliferators by making bomb

ingredients harder to get, more conspicuous to try to get, and

politically costlier to be caught trying to get. This would make

proliferation far more diffi cult, and easier to detect in time by

focusing scarce intelligence resources on needles, not haystacks.

Nuclear power has other unique challenges too, such as long-lived

radioactive wastes, potential for catastrophic accidents, and

vulnerability to terrorist attacks. But in a market economy, the

technology couldn’t proceed even if it lacked those issues, so we

needn’t consider them here.

Conclusion

So why do otherwise well-informed

people still consider nuclear power a key element of a sound climate

strategy? Not because that belief can withstand analytic scrutiny.

Rather, it seems, because of a superficially attractive story, an

immensely powerful and effective lobby, a new generation who forgot or

never knew why nuclear power failed previously (almost nothing has

changed), sympathetic leaders of nearly all main governments, deeply

rooted habits and rules that favor giant power plants over distributed

solutions and enlarged supply over efficient use, the market winners’

absence from many official databases (which often count only big plants

owned by utilities), and lazy reporting by an unduly credulous press.

Isn’t it time we forgot about nuclear power? Informed capitalists

have. Politicians and pundits should too. After more than half a

century of devoted effort and a half-trillion dollars of public

subsidies, nuclear power still can’t make its way in the market. If we

accept that unequivocal verdict, we can at last get on with the best

buys first: proven and ample ways to save more carbon per dollar,

faster, more surely, more securely, and with wider consensus. As often

before, the biggest key to a sound climate and security strategy is to

take market economics seriously.

Mr. Lovins, a physicist, is cofounder, Chairman, and Chief

Scientist of Rocky Mountain Institute, where Mr. Sheikh is a Research

Analyst and Dr. Markevich is a Vice President. Mr. Lovins has consulted

for scores of electric utilities, many of them nuclear operators. The

authors are grateful to their colleague Dr. Joel Swisher PE for

insightful comments and to many cited and uncited sources for research

help. A technical paper preprinted for the September 2008 Ambio (Royal

Swedish Academy of Sciences) supports this summary with full details

and documentation (www.rmi.org/sitepages/ pid257.php#E08-01).

RMI’s annual compilation of global micropower data from industrial and

governmental sources has been updated through 2006, and in many cases

through 2007, at www.rmi. org/sitepages/pid256.php#E05-04.

Notes:

-

This is conservatively used as the basis for all comparisons in this

article. The ~2-3¢/kWh nuclear "production costs" often quoted are the

bare operating costs of old plants, excluding their construction and

delivery costs (which are higher today), and under cheap old fuel

contracts that are expected to rise by several-fold when most of them

expire around 2012.

- All monetary values in this article are in 2007 U.S. dollars.

All values are approximate and representative of the respective U.S.

technologies in 2007. Capital and operating costs are levelized over

the lifespan of the capital investment.

- Distributed generators may rely on the power grid for emergency

backup power, but such backup capacity, being rarely used, doesn't

require a marginal expansion of grid capacity, as does the construction

of new centralized power plants. Indeed, in ordinary operation,

diversified distributed generators free up grid capacity for other

users.

- Solar power is not included in Figure 1 because the delivered

cost of solar electricity varies greatly by installation type and

financing method. As shown in Figure 4, photovoltaics are currently one

of the smaller sources of renewable electricity, and solar thermal

power generation is even smaller.

- A similar credit for displaced boiler fuel can even enable this

technology to produce electricity at negative net cost. The graph

conservatively omits such credit (which is very site-specific) and

shows a typical positive selling price.

- We ignore here the modest and broadly comparable amounts of

energy needed to build any kind of electric generator, as well as

possible long-run energy use for nuclear waste management or for

extracting uranium from low-grade sources.

- Since its recovered heat displaces boiler fuel, cogeneration

displaces more carbon emissions per kilowatt-hour than a large

gas- red power plant does.

- However, at long-run gas prices below those assumed here (a

levelized 2007-$ cost of $7.72 per million BTU, equivalent to assuming

that this price escalates indefinitely by 5%/y beyond

inflation-yielding prices far above the $7-10 recently forecast by the

Chairman of Chesapeake, the leading independent U.S. gas producer) and

at today's high nuclear costs, the combined-cycle plants may save more

carbon per dollar than nuclear plants do. This may also be true even at

the prices assumed here, if one properly counts combined-cycle plants

ability to load-follow, thus complementing and enabling cleaner,

cheaper variable renewable resources like windpower. Natural gas could

become scarce and costly only if its own efficiency opportunities

continue to be largely ignored. RMI's 2004 study Winning the Oil

Endgame (www.oilendgame.com)

found, and further in-house research confirmed in detail, that the US

could save at least half its projected 2025 gas use at an average cost

roughly one-tenth of the current gas price. Two-thirds of the potential

savings come from efficient use of electricity and would be more than

paid for by the capacity value of reducing electric loads.

- Data for decentralized gas turbines and diesel generators exclude generators of less than 1 megawatt capacity.

Correction: April 28, 2008

Due to new data, footnote 1 and 8 have been edited to reflect this new information.

Fair Use Notice.